On February 24, 2022, Russian President Vladimir Putin organized and initiated an invasion into Ukraine.

As of this writing, Russian forces continue war efforts to penetrate further into Ukraine and the geopolitical situation across Europe has already begun to shift in response; many trading partners have announced new sanctions and restrictions on Russian goods.

This continues to be a highly fluid situation, and dynamics on the ground are changing rapidly.

While the humanitarian implications are top of mind, the invasion is also impacting manufacturing operations and trade flows across the globe. The regional pulp & paper industry is expecting to undergo periods of extreme volatility as a result.

Eduard Litvak, Managing Director of the Ukrainian Pulp and Paper Industry Association UkrPapir, announced recently that all Ukrainian pulp and paper companies have halted production. Litvak explained that the military operations occurring throughout the country have led to a breakdown in logistics and supply chains and out of concern for the safety of employees, regional mills will be temporarily closed.

In addition to developments directly impacting the Ukrainian Pulp and Paper industry, major players within the industry have also made announcements and modifications over the last few weeks regarding the future of their operations in response to the conflict. Below is a brief timeline of some of these announcements:

- February 28: Mondi enforces a temporary suspension of production in Ukraine. Mondi has one paper bag plant located in Lviv, Ukraine which has been suspended as they continue to closely monitor the situation.

- March 1: Kemira discontinues all chemical sales and deliveries to Russia and Belarus – which will primarily impact pulp and paper consumers in Russia. In 2021, Russia represented around 3% of Kemira’s total revenue. This discontinuation will have a direct impact on production in Russia since Kemira has a strong position and involvement in some key chemicals like bleaching. With no bleaching chemicals, some mills will be forced to reduce production or switch to producing unbleached papers.

- March 2: Stora Enso stops all operations in Russia. Stora Enso has three corrugated packaging plants and two wood products sawmills in Russia. The company will also stop all exports and imports to and from Russia, however, a mitigation plan has been activated to secure availability of input materials from other sources.

- March 3: UPM ceases deliveries to Russia. While UPM has employees, customers, and suppliers in both countries, its exposure to Russian and Ukrainian markets is limited. UPM’s sales volume to Russa and Ukraine combined was approximately 2% of total sales in 2021.

- March 7: Sylvamo suspends Russian operations. The suspension focuses on employee and contractor safety and environmental stewardship. Sylvamo will continue to assess various options for its operations in Russia, which could include sale or exit.

- March 8: MM halts all carton deliveries to Russia.

- March 11: International Paper announces it may sell its 50% stake in major Russian forest products company Ilim Group. While International Paper has no intention to suspend its operations or initiate any liquidation or bankruptcy proceedings in regard to Ilim Group, it has started to explore strategic options which could include possibly selling its stake.

- March 18: Arkhangelsk Pulp and Paper Mill (APPM), a Pulp Mill Holding company in Russia, and its subsidiaries continue to operate their manufacturing and processing plants. In a statement, the company emphasizes that all commitments to employees, customers and partners will be fulfilled

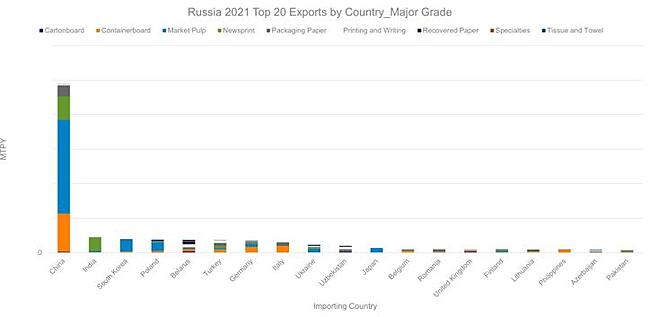

As a result of these suspended operations, certain P&P trade partners may experience a shift in operations. As illustrated in the chart below, Russian pulp and paper manufacturers exported a vast majority of their 2021 production to China, which received roughly 2,000,000 more MTPY than India – the second leading importer. With market pulp, containerboard and newsprint making up the top three exported grades to China, it is likely that China’s pulp and paper industry will experience considerable impacts as a result of Russia’s invasion and will potentially have to source those grades elsewhere.

However, most of the other top 20 trade partners will likely experience only a slight change in imports.

Source: FisherSolve Next

Source: FisherSolve Next

Russian paper producers are currently having issues with logistics, as many networks are partially non-operational due to the suspension of many international operators who traditionally handle Russian freight. The same problem is occurring with payment systems, as some Russian banks are now isolated from international transactions.

Russia, Belarus and Ukraine have been importing some paper products from Europe — mainly boxboard grades like FBB. Supply/demand of boxboard has been extremely tight recently and export to these countries will decrease as many European producers have pulled away from Russian and Belarus markets. Demand in Ukraine has also likely ceased due to the invasion, which will help the EU’s supply/demand balance. However, this is not occurring in the uncoated woodfree papers sector, as Russia is still exporting to Europe to meet current demand, which is at an all-time historical high.

Along with direct impacts to the pulp and paper industry, this ongoing conflict has created significant trade issues in other sectors as well, especially global energy, oil and gas markets. The world is now facing an extraordinary energy crisis, and there are no simple solutions close at hand. As oilprice.com recently wrote, “Oil prices and energy stocks are trading at multi-year highs after international refiners adopted a self-imposed embargo, with many reluctant to buy Russian oil and banks refusing to finance shipments of Russian raw materials. Refiners and banks are unwilling to do business with Russia due to the risk of falling under complex restrictions in different jurisdictions. Market participants are also concerned about measures directly targeting oil exports.”

As noted above, this is a highly fluid situation and dynamics across the pulp, paper and energy sectors will continue to change quickly. For additional insight into the possible impacts and disruptions this conflict could have on specific P&P segments, talk with an expert at Fisher International today.

Source: Fisher International