The global forest industry has experienced some serious changes across the past year. As we saw in our 2022 global forest industry predictions post, lots of volatility and global unrest yielded both expected and unexpected shifts.

What does the road ahead in 2023 look like? As is now an annual tradition, Forest2Market has compiled our top 6 predictions on what to expect in terms of the 2023 global forest industry.

1. North American lumber prices and demand will drop.

Up to when the Fed started putting the screws to the housing market, lumber prices enjoyed a historical run. Prices increased to record highs, and they kept hitting and breaking those records while home construction surged.

Those record lumber prices also turned into record sawmill profits and a flurry of new sawmill investments. Over the past few years, the US South alone added 5 billion board feet (BBF) of production, equating to a 20% increase in capacity.

Increasing housing starts and the so-called “COVID Bubble” also sent lumber demand through the roof. In 2023, this will all come to an end. Slower housing demand, coupled with abundant lumber supply, will send lumber prices to the $350/MBF range – exacting pain on the industry.

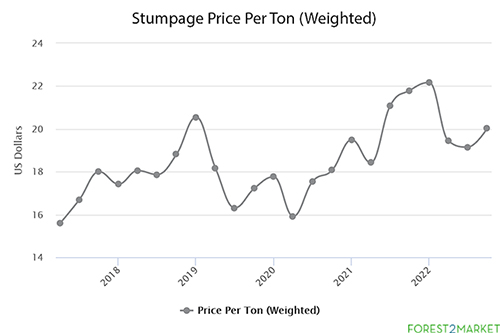

2. Stumpage prices will decline for logs in the US South and increase slightly in the PNW, while pulpwood will remain regionally strong.

Demand for sawlogs will decrease across the nation because of slack housing demand. In the South, where logs are still in plentiful supply, prices will trend down.

As the stumpage price per ton trends show (see line graph), a big dip at the start of 2022 did recover by year end. However, expect declines in prices in the coming months.

In the NW US, log pricing will remain at its elevated state. China will demand more logs as it emerges from strict COVID lockdowns. They will first turn to BC and then to the PNW, competing with domestic producers who will already be in a price squeeze between low lumber prices and expensive logs.

3. The Inflation Reduction Act will focus investments on renewables, but little will occur besides planning, studies, and the like.

With the passage of the Inflation Reduction Act (IRA), the US Federal Government has unleashed a torrent of investment in renewable energy – specifically sustainable aviation fuel (SAF).

The energy – pun totally intended – around SAF has many big backers. The largest airlines are counting on SAF to underwrite their green credentials by underwriting these green investments with long-term, multi-billion-dollar fuel offtake agreements.

Biden’s Sustainable Aviation Fuel Target grand challenge and the entire EU complex is chomping at the bit to reduce greenhouse gases and ready to throw money at it. The lucrative subsidies provided in the IRA are an important catalyst. So ultimately, little will happen this year other than a massive investment in site diligence, engineering, project planning and other studies.

4. The pulp and paper industry will underestimate or even dismiss the SAF market in the US.

Related to SAF, this prediction is much like 2007 within the pellet industry.

The US forest products industry dismissed UK legislation even though subsidies were memorized and lucrative (very similar to the IRA). Projected demand for wood pellets was astonishingly high. Some initially predicted that 50 million tons of pellets would be exported from the US to Europe.

AS we now know, of course, they were wrong. Only 12 million tons of pellets are now exported across more than 20 large production facilities and a myriad of dedicated ports and logistics hubs.

We hear the same arguments today relative to SAF that were made in 2007 against pellets:

- It’s subsidized.

- It’s too expensive.

- It will never replace a large portion of fossil-derived aviation fuel.

We will see if it ultimately matters. History has already told us differently.

5. US and European pulp markets will feel the effects of a recession, while Latin America will benefit.

The pulp industry in Europe will continue to face challenges. Alongside higher energy costs, waning demand for pulp and paper due to an impending recession will result in a difficult year for the European industry. The US industry will be right behind.

Latin American producers on the other hand will continue to benefit from the weak US dollar and euro and lower costs due to smart investments in large pulp mills. The lowest cost producer almost always wins!

6. The death of forest carbon credits is coming.

As much as I love the fact that forests are now recognized for their carbon benefit, the jig is up.

Firstly, the general move away from carbon credits is damaging forest carbon markets. The world is coming around to the fact that carbon credits, of any kind, are just a license to pollute more.

Secondly, the carbon is stored longer in the finished product, especially lumber and cross-laminated timber. And it is certainly simpler to measure these amounts.

Delaying harvests and getting paid for the carbon stored on the stump works until the tree dies. But this raises an obvious question: then what?

Source: Forest2Market