In 2023, the pulp, paper, and forest industries navigated through a series of dynamic market shifts and unanticipated challenges.

From fluctuations in demand and prices to a growing focus on biofuel possibilities, the sector experienced noteworthy transformations.

As per our annual tradition, ResourceWise is pleased to present our top insights and forecasts for the pulp, paper, and forest products industry in 2024. Here are five key predictions shaping the upcoming year.

2024 Predictions

- The inventory destocking that occurred in virtually every industry in 2023 is coming to an end. This brings positive implications for the global pulp and paper industry and solid wood and lumber markets. Inventory destocking was one of the more important factors that contributed to the 2023 economy. With the end of destocking and indications of the Federal Reserve’s interest rate hikes ending, confidence in the economy has been embedded. This sets the stage for a resurgence in economic activity within the industrial sector, which is expected to occur in the first quarter of 2024.

- Most new forestry investments in 2024 will be concentrated in the US South. The forests in the US South, including North Carolina, boast incredible productivity and offer some of the most cost-effective fiber in the world. As we look ahead to 2024, landowners may hope for a surge in log and fiber prices, but unfortunately, the supply and demand balance is weighted towards too much supply. However, there is a silver lining to this. The low cost of log fiber serves as an incentive for new manufacturing, increasing the demand for logs and fiber.

- Housing starts will be relatively strong in 2024, hanging between 1.3–1.5 mm starts. In addition, demand for engineered wood—CLT, glulam, I-Joists, and mass timber—will continue to build, underpinning sawlog demand.

- Increase in investment in bio-economy production at pulp mills. Driven by governmental regulations such as the Green New Deal in the EU and supported by incentives like the Inflation Reduction Act, we anticipate a surge in investments to produce low-carbon biogenic fuels, chemicals, and materials. The significant amount of biogenic carbon dioxide generated by pulp mills, combined with growing consumer demand and government support, will fuel this investment trend. If these markets develop economically, we see the potential for pulp assets globally, but especially in North America, to be revalued.

- Are Pulp and Paper Companies Sitting on a Hidden Goldmine?

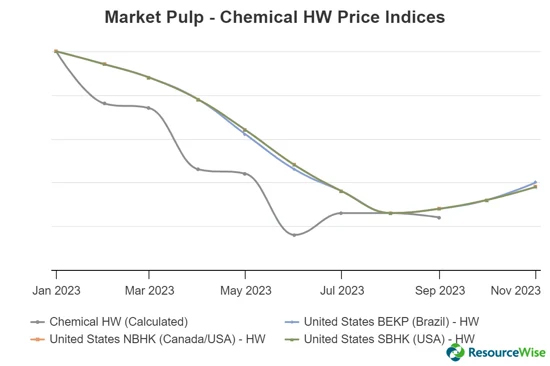

- Are Pulp and Paper Producers Missing the Profitable Opportunities CTO Has to Offer? - Global operating rates in the pulp and paper industry will continue to improve, bringing stability to the sector. Following a period of sluggish growth and declining prices, we are now witnessing promising signs of a market upturn. For example, when looking at the price trend of hardwood market pulp in the United States, we can see that prices began to rise in the fall of 2023. A similar trend was also seen in countries such as China, Brazil, and India.

To restore equilibrium between supply and demand, struggling mills, particularly in free-market economies, have been forced to shutter. However, China's operating rates will likely remain lower in the upcoming year and potentially for several years to come. Industry experts attribute these gradual price increases to the implementation of recycled fiber mill projects and a steady rise in overall demand for fiber in North America.

Despite the possibility of ongoing fluctuations in the near future, we are optimistic to see what lies ahead for the pulp, paper, and forestry industries in 2024. To stay updated on all the latest discussions surrounding the global forest products industry, be sure to subscribe to our weekly blog updates.

Source: ResourceWise